Atlassian (TEAM +15.48%) developed a collection of software program merchandise designed to foster collaboration and productiveness for its enterprise prospects. There’s Jira, which helps software program growth groups handle their initiatives, after which there may be Confluence, which is a digital city sq. the place workers can talk about work and share operational updates.

Atlassian inventory was buying and selling at over $300 originally of 2025, till Wall Road shaped the view that synthetic intelligence (AI) was about to decimate the software program trade. In consequence, by April this yr, the inventory had fallen to as little as $57.

That is once I bought , and I added it to my portfolio at round $58. I haven’t got a crystal ball; I merely felt Wall Road was overreacting to the potential risk of AI, particularly as a result of Atlassian was efficiently utilizing it to make more cash. The inventory has since rocketed 83% larger and closed at $107 on Friday, Might 29. Here is why I believe considerably extra upside is forward.

Picture supply: Getty Photographs.

AI is definitely serving to Atlassian’s enterprise

Wall Road thought AI was a risk to software program firms for 2 causes. First, analysts thought instruments comparable to Anthropic’s Claude Code would enable companies to develop their very own variations of merchandise comparable to Jira and Confluence, making firms like Atlassian redundant. Second, if AI resulted in widespread job losses, the Road felt software program firms with seat-based income fashions would lose a bit of their revenue.

To counter the primary challenge, Atlassian does not simply promote software program. It gives the safety, infrastructure, and technical help required to deploy Jira and Confluence efficiently. These items price a ton of cash to arrange and preserve, which is simply worthwhile at scale. In different phrases, the typical enterprise would possibly be capable of clone Jira and Confluence utilizing an AI coding assistant, however stopping information breaches and sustaining uptime is an entire different problem.

Plus, Atlassian developed its personal AI platform known as Rovo, which comes with a whole suite of options to reinforce the capabilities of Jira and Confluence. It contains a complicated search device that may immediately find data from throughout the group, even when it is not saved inside the Atlassian ecosystem. Rovo also can function a coding assistant to assist software program builders speed up their workflows, which is the final word addition to a product like Jira.

Greater than 350,000 companies worldwide use Atlassian, so the corporate has a treasure trove of information with which to enhance its AI fashions. This benefit makes Rovo extra helpful than most generic AI assistants, which additional entrenches the Atlassian software program ecosystem deeper into every group.

Now, on to Wall Road’s second concern.

A shock acceleration in income development

Atlassian generated $1.8 billion in complete income throughout its fiscal 2026 third quarter (ended March 31), which blew away Wall Road’s estimate of $1.7 billion. It was a 32% enhance from the year-ago interval, marking a pointy acceleration from the 23% development the corporate delivered three months earlier within the second quarter. That alone squashed considerations that AI was inflicting a loss in income for software program firms.

In actual fact, Atlassian stated annual recurring income (ARR) from Rovo prospects grew at twice the tempo of ARR from non-Rovo prospects. So, once more, AI is proving to be a large tailwind for this firm, not a risk.

In the present day’s Change

(15.48%) $14.44

Present Worth

$107.73

Key Knowledge Factors

Market Cap

$27B

Day’s Vary

$97.44 – $108.48

52wk Vary

$56.01 – $222.59

Quantity

987

Avg Vol

7.4M

Gross Margin

84.50%

To ease considerations even additional, Atlassian launched a brand new pricing choice for purchasers on Might 6. It is known as Flex, and it permits enterprises to set a finances they’ll allocate to any Atlassian merchandise throughout their contract interval, with out having to barter new phrases. The corporate calls it a value-based pricing mannequin, as a result of prospects are paying based mostly on what they use, not what number of seats, or customers, they may have inside a selected time-frame.

Flex will make it considerably simpler for brand new prospects to stand up and working with Atlassian, which may drive additional momentum on the high line. Cybersecurity big CrowdStrike launched an analogous versatile subscription choice in 2023, and it continues to gas an acceleration within the firm’s income development to at the present time.

Why Atlassian nonetheless has room to run

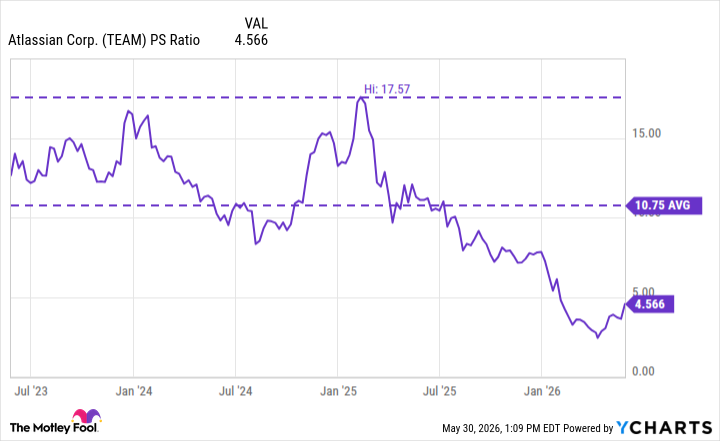

Regardless of the blistering features in Atlassian inventory since April, it is nonetheless buying and selling at a price-to-sales (P/S) ratio of simply 4.5 — far beneath its three-year common of 10.7, and even additional beneath final yr’s peak of 17.5.

TEAM PS Ratio information by YCharts

Atlassian inventory must soar by 137% from final Friday’s shut simply to match its three-year common P/S ratio, which I believe is completely potential contemplating the corporate’s accelerating income development. That will lead to a inventory worth of $255.

However I intend to carry the inventory past that time, as a result of I believe the corporate is getting into an period of quicker development and innovation because it capitalizes on the AI alternative over the following few years.