India’s wires and cables companies have delivered sturdy returns over the previous few months. The sector contributes practically 40-45% of India’s electrical industry, making it one of many key pillars of the nation’s industrial and infrastructure ecosystem.

For years, progress was largely pushed by infrastructure, power, real estate, and government-led capex. However a brand new alternative is now rising. Dawn sectors similar to data centres, electric vehicles, renewable energy, and defence manufacturing are starting to reshape demand for the business.

These sectors require high-voltage, fast-charging, fibre-optic, and structured cabling options. On the identical time, the fast adoption of AI, cloud computing, and 5G is accelerating the enlargement of information centres throughout India. That is making a contemporary demand cycle for specialised cables and high-speed transmission techniques.

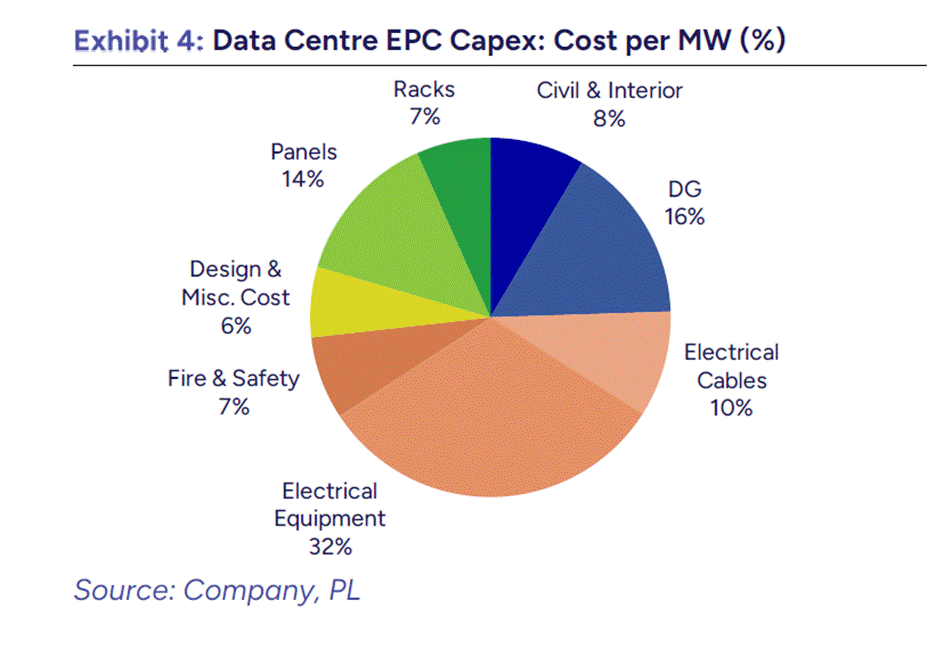

As per Prabhudas Lilladher Capital, electrical cables account for practically 10% of the full price per megawatt (MW) in knowledge centre tasks. With EPC prices estimated at ₹ 20.0–22.5 crore per MW, the cable alternative turns into sizeable as capacities develop.

India’s knowledge centre capability is projected to rise from 1,337 MW in FY25 to three,395 MW by FY30, implying an addition of two,058 MW over the subsequent 5 years. This interprets into an estimated complete EPC alternative measurement of practically ₹46,400 crore. Of this, the wires and cables sector (10%) may seize round ₹4,600 crore, or ₹927 crore yearly.

Electrical Cable Accounts for 10% of Knowledge Middle EPC Capex

In the meantime, the wires and cables business is projected to develop from ₹90,000 crore in FY25 to ₹1,57,500 crore in FY30, positioning it as a quickly increasing sector. In opposition to this backdrop, this text examines three market leaders that unveil sturdy enlargement plans to capitalize on upcoming progress alternatives.

#1 R R Kabel: The Further Excessive Voltage Progress Play

R R Kabel manufactures electrical goods, particularly Wires & Cables and Quick Shifting Electrical Items (FMEG). It has crossed the US$ 1 billion income milestone, reaching its highest-ever annual income of ₹9,722 crore in FY26.

The Wires and Cables section is the expansion driver, accounting for 90% of the full income in FY26. Inside this section, its product gross sales combine contains roughly 73% wires and 27% cables. Cable’s contribution to income is anticipated to extend to 31% from the present 27%.

The ₹1,200 Crore EHV Pivot: Shifting Up the Worth Chain

Presently, R R Kabel has the manufacturing functionality to provide cables as much as 66 KV. To seize extra worth, it’s executing a ₹1,200 crore CAPEX to fabricate Further Excessive Voltage (EHV) cables as much as 220 KV by FY28. This 220 KV functionality represents the decrease finish of the EHV section or the upper finish of the high-voltage cable spectrum.

Because the capability utilization exceeds 90%, including this new capability is essential to satisfy future progress necessities. Parts of the brand new 220 KV capability will begin going stay by the center and finish of FY27. All the capability is anticipated to be totally accomplished by FY28.

As soon as totally commissioned, this can allow quicker execution of B2B cable orders and higher operational leverage. The corporate plans so as to add new capacities progressively each six months.

Knowledge Middle Redundancy: A Huge B2B Progress Lever

Via this enlargement, R R Kabel goals to develop its B2B section by concentrating on quickly rising sectors similar to knowledge facilities. Administration views data centers as a “large sector” anticipated to see sturdy demand over the subsequent 3-4 years. Thus, knowledge facilities, together with wind and solar energy tasks, have been the first goal markets.

The Redundancy Premium: Why AI Infrastructure Requires Huge Over-Cabling

Knowledge middle operators can’t afford even a 0.01% failure in energy. To make sure this reliability, these services usually characteristic 4 or 5 redundant energy backup techniques. These techniques require large volumes of wiring and cabling all through the infrastructure.

The corporate is actively making ready to seize this incoming demand.

The corporate is at the moment approaching knowledge middle clients to safe the required product approvals. They plan to cater to this market utilizing a blended method, supplying each on to the tip clients and thru their established distribution networks.

It tasks 16-18% year-over-year quantity progress (above business common), pushed by scaling its B2B enterprise.

The Center East Export Hurdle

In FY26, the corporate derived 74% of its income from the Indian market and 26% from international exports. In comparison with its opponents, R R Kabel has a considerably greater reliance on exports. Round 30% of its income from its wires and cables enterprise comes from exports. Of this, the Center East accounted for 40%, representing 12% of the general prime line.

As a result of this excessive income publicity, it’s prone to expertise short-term damaging impacts on export revenues in Q1FY27. Nonetheless, the corporate stays assured that its presence in different international markets will assist mitigate this influence over the long run.

B2C to B2B Transition: RR Kabel’s Technique for 18% Quantity Progress

To maintain its operations, the corporate is at the moment guided by a 3-year strategic roadmap referred to as “Undertaking RRise”. Via this initiative, R R Kabel focuses on deepening buyer engagement, increasing its international footprint, and growing efficiencies. Its objective is to attain an 18% CAGR in wire and cable quantity.

From a monetary perspective, the corporate’s income grew 28% year-on-year to ₹9,722 crore, pushed by 31% progress in Wires and Cables income to ₹8,764 crore. EBITDA rose 62% to ₹789 crore, whereas margins expanded by 171 foundation factors to eight.1%, pushed by economies of scale. Because of this, internet revenue surged by 58% to ₹492 crore.

For dividend hunters, it additionally paid a complete dividend of ₹9.5 in FY26, together with a ultimate dividend of ₹5.5 per share introduced throughout Q4FY26 earnings. This interprets to a dividend yield of 0.5%. That is low in comparison with a 3.7% yield offered by this zero-debt PSU.

#2 Polycab: From Market Chief to Knowledge Middle Enabler

Polycab is the most important firm within the Indian electrical business by income. The corporate manufactures and sells electrical merchandise. Wires & Cables is the corporate’s core enterprise and largest section. Polycab holds 30% market share within the organised wires and cables business in India.

Dominating the Core: Polycab’s ₹25,000 Crore Wires & Cables Engine

The corporate reported its highest-ever consolidated income of ₹28,884 crore in FY26. The Wires and Cables section continues to be the dominant contributor, producing ₹ 25,179 crore in FY26 (accounting for roughly 87% of the full income).

The FMEG section contributes 8%. The home market accounts for nearly 95% of its enterprise. Polycab’s enterprise mannequin closely leans on its distribution channel. They account for about 90% of its gross sales, with institutional (B2B/tender) gross sales making up the remaining 10%.

The Knowledge Middle Pivot: Tapping into AI-Pushed Demand Pockets

Knowledge facilities symbolize a key structural progress driver for Polycab, notably inside its Wires & Cables enterprise section. The corporate has strategically positioned its merchandise to play a vital function in high-growth sectors, together with knowledge facilities, renewable power, metro rail, and superior manufacturing.

Undertaking Spring: Scaling CAPEX to ₹8,000 Crore for FY30 Targets

Polycab’s administration particularly highlighted knowledge facilities and artificial intelligence-driven demand as “new demand pockets” which can be but to completely bloom.

As well as, the rising sectors, alongside defence and EV charging networks, are anticipated to develop considerably and generate sustained, sturdy demand over the approaching years.

The corporate estimates that the projected CAPEX (public + non-public) of roughly ₹36 lakh crore in FY27 will translate into sturdy demand for cables and wires. Polycab can be making ready to capitalize on knowledge middle alternatives.

Polycab is already offering specialised options for big knowledge middle tasks, together with Vodafone Thought’s knowledge facilities.

Polycab’s administration has laid out clear monetary and operational targets to be achieved by the tip of the FY30 beneath its “Undertaking Spring” technique. The corporate goals to outpace the business by rising each its Wires & Cables and FMEG segments at 1.5x to 2x the market progress charge.

It additionally intends to lift the dividend payout to over 30%, up from 27.2%.

FY26 Monetary Assessment: Margin Growth Amidst File Income

To assist this progress, Polycab has dedicated a CAPEX of ₹6,000-8,000 crore over the subsequent 5 years. Roughly 90% of this will likely be directed towards increasing Wires & Cables capability. Like R R Kabel, a brand new Further Excessive Voltage capability is on observe to be commissioned by the tip of 2027 and can begin contributing to revenues in FY28.

From a monetary perspective, Polycab FY26 income grew 29% year-on-year to ₹28,884 crore, pushed by 33% progress in Wires and Cables income. EBITDA rose 35% to ₹4,006 crore, whereas margins expanded by 70 bps to 13.9%.

Working leverage and a good product combine shift drove this enlargement. Because of this, internet revenue surged by 32% to ₹2,708 crore.

#3 KEI Industries: Betting on Exports and Excessive-Voltage Progress

KEI Industries manufactures wire and cable for each institutional (B2B) and retail (B2C) markets.

The Integration Benefit: Scaling Past Customary Wires

Its particular cable and wire merchandise embody Further Excessive Voltage, Excessive Rigidity, and Low Rigidity Cables. Along with commonplace cables, KEI manufactures and sells chrome steel wires.

KEI additionally operates an EPC division, however it’s strategically a supporting enterprise relatively than a progress engine. The EPC division primarily helps its extra-high-voltage cable tasks, the place the worth of the cables accounts for greater than 80% of the challenge worth.

Backward Integration: Defending the Backside Line

To assist its cable manufacturing, KEI engages in backward integration by manufacturing a few of its personal uncooked supplies. It manufactures PVC compounds and low-tension XLP compounds. The corporate can be planning future tasks to fabricate its personal medium-voltage compounds and galvanized metal wire for cable armoring.

Like R R Kabel and Polycab, knowledge facilities additionally symbolize a major and rising driver of demand for KEI. Administration has highlighted the enlargement of information facilities as a significant catalyst for sturdy demand. Internationally, knowledge facilities are anticipated to be a “huge booster” for KEI’s export enterprise, notably within the American market.

The US Export Rebound: Navigating Tariffs and Knowledge Middle Demand

Following a short lived slowdown in FY26 as a result of US tariffs, KEI has efficiently resumed its export operations to the US. It anticipates that knowledge middle tasks will assist drive substantial gross sales within the area. The corporate primarily expects to produce medium-voltage HD (Excessive Rigidity) cables, in addition to some versatile copper cables, to satisfy knowledge middle wants.

KEI is actively evaluating its portfolio to establish further cable varieties it could introduce for knowledge middle tasks. Nonetheless, administration acknowledges that increasing their product footprint on this particular sector is difficult, as they face stiff competitors from the established American home cable manufacturing business.

Sanand Growth: The Roadmap to twenty% Quantity Progress in FY28

To spice up its progress, KEI is investing in increasing its manufacturing community. The primary section of the Sanand plant was commissioned in December 2025. The second section is anticipated to be accomplished by Q4FY27. The corporate anticipates quantity progress of 17-18% in FY27 and tasks progress of as much as 20% in FY28 following the completion of the second section of the Sanand plant.

Monetary Efficiency: Margin Growth Amidst File Income

From a monetary perspective, KEI income grew 21% year-on-year to ₹11,748 crore in FY26, pushed by 32% worth progress within the wire and cable section. EBITDA rose 31% to ₹1,388 crore, whereas margins grew by 89 bps to 11.8%, pushed by a good product combine shift towards exports and B2C gross sales. Because of this, internet revenue surged by 32% to ₹918 crore.

Valuation Hole: Are Wires and Cables Shares Buying and selling at a Low cost?

With superior progress and profitability, Polycab leads the return ratios (Return on Capital Employed and Return on Fairness) chart, adopted by R R Kabel and KEI. All three corporations, as business leaders, are buying and selling at a premium to the business median. R R Kabel, nevertheless, trades at a slight low cost to 3-year historic median, whereas Polycab and KEI commerce at a premium.

| Valuation Comparability (X) | ||||

| Worth-to-Earnings A number of | Return Ratios | |||

| Firm | Firm | 3Y Median | ROCE (%) | ROE (%) |

| R R Kabel | 43.4 | 49.3 (2.7 Yrs) | 25.8 | 20.8 |

| Polycab | 51.2 | 47.8 | 34.3 | 24.5 |

| KEI Industries | 53.1 | 51.4 | 20.1 | 14.8 |

| Trade Median | 25.6 | 20.3 | 18.9 | |

India’s wires and cables business, already valued at practically ₹90,000 crore, is anticipated to succeed in ₹1,57,500 crore by FY30. With India’s knowledge centre capability projected to develop from 1,337 MW to three,395 MW by FY30, corporations increasing into EHV cables, exports, and B2B options may emerge as key beneficiaries of this subsequent progress cycle.

Nonetheless, within the quick time period, uncooked materials costs may threaten margins and profitability. The important thing dangers to be careful for embody uncooked materials costs for copper, aluminum, oil, and PVC. That mentioned,keep these stocks on your watchlist to see how they faucet into the info middle demand.

Disclaimer

Word: All through this text, now we have relied on knowledge from http://www.Screener.in and the corporate’s investor presentation. Solely in instances the place the info have been unavailable have we used an alternate, broadly accepted, and broadly used supply of data.

The aim of this text is just to share attention-grabbing charts, knowledge factors, and thought-provoking opinions. It’s NOT a advice. Should you want to take into account an funding, you might be strongly suggested to seek the advice of your advisor. This text is strictly for instructional functions solely.

In regards to the Creator: Madhvendra has been deeply immersed within the fairness markets for over seven years, combining his ardour for investing along with his experience in monetary writing. With a knack for simplifying advanced ideas, he enjoys sharing his sincere views on startups, listed Indian corporations, and macroeconomic traits.

A devoted reader and storyteller, Madhvendra thrives on uncovering insights that encourage his viewers to deepen their understanding of the monetary world.

Disclosure: The author and his dependents don’t maintain the shares mentioned on this article. The web site managers, its worker(s), and contributors/writers/authors of articles have or might have an excellent purchase or promote place or holding within the securities, choices on securities, or different associated investments of issuers and/or corporations mentioned therein. The articles’ content material and knowledge interpretation are solely the private views of the contributors/ writers/authors. Traders should make their very own funding selections primarily based on their particular aims, assets, and solely after consulting such unbiased advisors as could also be mandatory.