Key Takeaways

- IBM is seen as the higher AI tech choose now, regardless of lagging Qualcomm’s past-year beneficial properties.

- IBM added Mixtral-8x7B to watsonx, citing 50% greater throughput and potential 35%-75% latency cuts.

- QCOM is pushing on-device gen AI and auto/edge chips, however faces Intel rivalry and stock drag.

Worldwide Enterprise Machines Company (IBM – Free Report) and Qualcomm Included (QCOM – Free Report) are legacy tech behemoths aggressively increasing into AI infrastructure and enterprise AI options, with rising publicity to edge computing and next-generation AI workloads. IBM presents cloud and information options that assist enterprises in digital transformation. Along with hybrid cloud providers, the corporate gives superior data know-how options, pc programs, quantum computing and supercomputing options, enterprise software program, storage programs and microelectronics.

Qualcomm presents high-performance, low-power chip designs for cellular units, PCs, XR (Prolonged Actuality), automotive, wearable, robotics, connectivity and AI use circumstances. The corporate boasts a complete mental property portfolio comprising 4G, 5G and different applied sciences. Qualcomm’s manufacturers embody Snapdragon systems-on-chip, FastConnect Wi-Fi and Bluetooth programs, and Qualcomm-branded 4G, 5G and IOT tools. The corporate is at present integrating on-device generative AI into all of its product strains.

Allow us to delve a bit of deeper into the businesses’ aggressive dynamics to grasp which of the 2 is comparatively higher positioned within the trade to warrant a spot in your funding portfolio.

The Case for IBM

IBM is poised to learn from wholesome demand traits for hybrid cloud and AI, which drive the Software program and Consulting segments. The corporate’s progress is predicted to be aided by analytics, cloud computing and safety in the long run. With a surge in conventional cloud-native workloads and related purposes, together with an increase in generative AI deployment, there’s a radical growth within the variety of cloud workloads that enterprises are at present managing. This has resulted in heterogeneous, dynamic and sophisticated infrastructure methods, which have led companies to undertake a cloud-agnostic and interoperable method to extremely safe multi-cloud administration, translating right into a wholesome demand for IBM hybrid cloud options.

IBM has built-in the open-source Mixtral-8x7B massive language mannequin into its watsonx AI and information platform. Mixtral-8x7B’s incorporation underscores IBM’s dedication to cutting-edge AI analysis and growth. Constructed on revolutionary Sparse modeling and the Combination-of-Specialists approach, this mannequin excels in speedy information processing and contextual evaluation. Its potential to effectively deal with huge datasets makes it a helpful asset for companies searching for actionable insights. The optimized model of Mixtral-8x7B, developed by Mistral AI, showcases spectacular efficiency beneficial properties. Inner exams reveal a exceptional 50% improve in throughput in comparison with the usual mannequin. By leveraging quantization strategies to cut back the mannequin measurement and reminiscence necessities, IBM anticipates important reductions in latency, doubtlessly starting from 35% to 75%, relying on batch measurement.

Regardless of strong hybrid cloud and AI traction, IBM is dealing with stiff competitors from Amazon.com, Inc.’s (AMZN – Free Report) AWS and Microsoft Company’s (MSFT – Free Report) Azure. Growing pricing strain is eroding margins, and profitability has trended down over time, barring occasional spikes. The corporate faces a potent risk from AI agency Anthropic because the latter’s Claude Code instrument can modernize legacy COBOL programs — a foundational programming language deeply embedded in IBM’s mainframe ecosystem. With Claude Code proposing to considerably automate code exploration, documentation, refactoring and safety evaluation, it threatened to cut back enterprises’ reliance on specialised legacy service suppliers like IBM, bringing its sustenance at stake.

The Case for QCOM

Qualcomm is well-positioned to satisfy its long-term income targets, pushed by strong 5G traction, higher visibility and a diversified income stream. The corporate is more and more specializing in the seamless transition from a wi-fi communications agency for the cellular trade to a linked processor firm for the clever edge. Qualcomm is witnessing wholesome traction in EDGE networking, which helps rework connectivity in automobiles, enterprise enterprises, properties, good factories, next-generation PCs, wearables and tablets. The automotive telematics and connectivity platforms, digital cockpit and C-V2X options are additionally fueling rising automotive trade traits resembling the expansion of linked autos, the transformation of the in-car expertise and car electrification.

Automakers are more and more deploying high-performance, low-power computing and connectivity chips to carry next-generation expertise to shoppers. Administration famous that greater than 1 million automobiles are working ADAS and autonomy on Snapdragon Experience processors, whereas indicating that business shipments of its next-generation digital chassis platform are anticipated to start by the top of the fiscal yr. The corporate is strengthening its foothold within the cellular chipsets market with revolutionary product launches. It had prolonged its Snapdragon G Collection portfolio with the addition of next-generation gaming chipsets, Snapdragon G3 Gen 3, Snapdragon G2 Gen 2 and Snapdragon G1 Gen 2 chips.

Regardless of efforts to ramp up its AI initiatives, Qualcomm has been dealing with robust competitors from Intel within the AI PC market. Shift within the share amongst OEMs on the premium tier has decreased Qualcomm’s near-term alternative to promote built-in chipsets from the Snapdragon platform. The corporate is impeded by reminiscence provide constraints and associated pricing, adversely impacting its handset revenues as OEMs (notably in China) continued to attract down channel stock. Administration reiterated that QCT handset revenues from China-based clients are anticipated to backside out within the fiscal third quarter and resume sequential progress within the following quarter because the stock drawdown eases.

How Do Zacks Estimates Evaluate for IBM & QCOM?

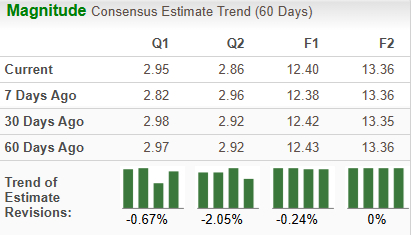

The Zacks Consensus Estimate for IBM’s 2026 gross sales implies a year-over-year rise of 5.9%, whereas that of EPS signifies progress of seven%. EPS estimates have been trending southward (down 0.2%) on common over the previous 60 days.

Picture Supply: Zacks Funding Analysis

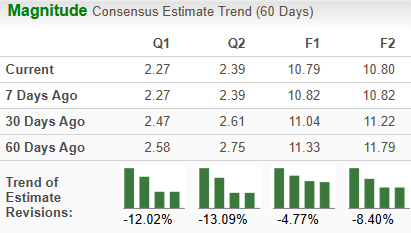

The Zacks Consensus Estimate for Qualcomm’s fiscal 2026 gross sales suggests a year-over-year fall of two.8%, whereas that for EPS implies a decline of 10.3%. The EPS estimates have been trending southward (down 4.8%) over the previous 60 days.

Picture Supply: Zacks Funding Analysis

Worth Efficiency & Valuation of IBM & QCOM

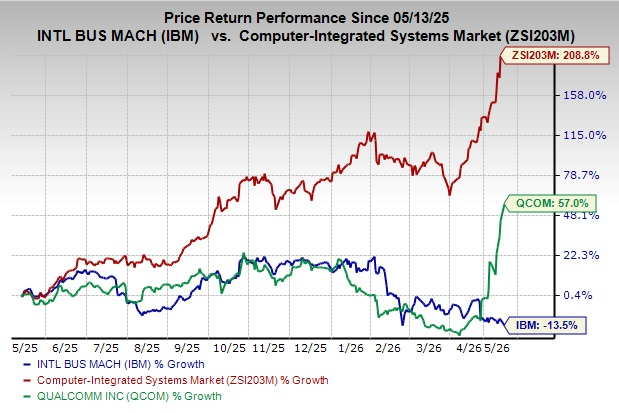

Over the previous yr, IBM has plunged 13.5% in opposition to the industry’s whopping progress of 208.9%. Qualcomm has gained 57% over the identical interval.

Picture Supply: Zacks Funding Analysis

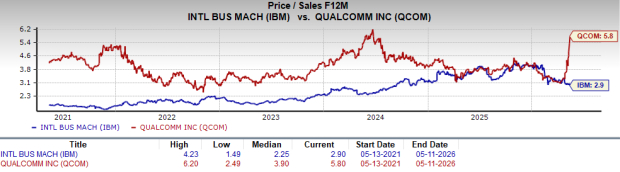

IBM appears to be like extra engaging than Qualcomm from a valuation standpoint. Going by the value/gross sales ratio, IBM’s shares at present commerce at 2.9 ahead gross sales, decrease than 5.8 for Qualcomm.

Picture Supply: Zacks Funding Analysis

IBM or QCOM: Which is a Higher Choose?

Each IBM and Qualcomm carry a Zacks Rank #3 (Maintain). You may see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Whereas IBM expects gross sales to enhance in 2026, Qualcomm expects revenues to lower yr over yr. Qualcomm has proven a comparatively regular income progress for years, whereas IBM has been dealing with a bumpy highway. IBM is buying and selling comparatively cheaply in contrast with Qualcomm, though it has lagged the latter by way of worth efficiency.

With a secure free money move and software-driven revenues leaning towards enterprise SaaS/AI transformation, IBM seems to be comparatively higher positioned than Qualcomm. Consequently, IBM appears to be a greater funding choice in the meanwhile.