Key Takeaways

- Salesforce is increasing past CRM, utilizing Slack and Informatica to construct an AI/knowledge ecosystem.

- Oracle plans practically $50B FY26 capex, with free money stream deeply detrimental in FY26.

- CRM trades at 12.76X ahead P/E, considerably decrease than Oracle’s 24.2.

Salesforce, Inc. (CRM – Free Report) and Oracle Company (ORCL – Free Report) are two of the most important gamers in enterprise cloud software program. Each firms are closely investing in synthetic intelligence (AI) and cloud infrastructure as companies proceed shifting extra operations to digital platforms.

Whereas Salesforce dominates buyer relationship administration software program, Oracle has grow to be a serious drive in cloud databases and AI infrastructure. Each are benefiting from the rising demand for AI-powered enterprise options, however they’re approaching the chance otherwise.

The important thing query for traders is easy: which firm provides the higher mixture of development, stability and valuation proper now? A better take a look at their companies, monetary tendencies and AI methods gives the reply.

The Case for Salesforce Inventory

Salesforce stays the clear chief in buyer relationship administration software program, a place it has maintained for years, in accordance with Gartner. However the firm’s story at the moment goes far past merely a buyer relationship administration software program supplier.

Salesforce is progressively remodeling itself right into a broader enterprise AI and knowledge platform. Its acquisitions of Slack and Informatica present administration’s intention to create an built-in ecosystem that mixes communication, automation, analytics and AI. Smaller acquisitions like Doti AI and Spindle AI additional spotlight how aggressively Salesforce is making an attempt to strengthen its AI capabilities.

AI has shortly grow to be one of many firm’s greatest development drivers. Since launching Einstein GPT in 2023, Salesforce has been embedding generative AI instruments throughout its platform to assist companies automate workflows, enhance productiveness and ship higher buyer experiences.

Its newer AI merchandise, particularly Agentforce and Information Cloud, are gaining sturdy traction. Collectively, these choices generated $2.9 billion in recurring revenues within the fourth quarter of fiscal 2026, marking greater than 200% year-over-year development. Agentforce alone contributed $800 million in recurring revenues, up 169% from the prior-year quarter. Importantly, greater than 60% of Agentforce offers got here from current clients, displaying Salesforce’s sturdy skill to promote further AI companies to its large put in base.

Monetary efficiency additionally stays strong. Within the fourth quarter of fiscal 2026, revenues elevated 12% 12 months over 12 months, whereas non-GAAP earnings per share jumped 37%. Each figures comfortably beat the Zacks Consensus Estimate, displaying that Salesforce continues to execute properly regardless of a difficult macroeconomic atmosphere.

The Case for Oracle Inventory

Oracle has additionally been delivering spectacular development, notably in cloud infrastructure. Within the third quarter of fiscal 2026, revenues rose 22% 12 months over 12 months to $17.2 billion, whereas non-GAAP EPS elevated 21% to $1.79.

The most important development engine for Oracle is its cloud infrastructure enterprise, which has grow to be more and more necessary as firms construct AI purposes and require large computing energy. Oracle’s cloud infrastructure revenues surged 84% 12 months over 12 months to $4.9 billion in the course of the quarter, whereas cloud utility revenues rose 13% to $4 billion.

Oracle’s multi-cloud technique is one other main power. The corporate is positioning its database companies to work seamlessly throughout a number of cloud suppliers, which helps appeal to enterprise clients. Within the third quarter, cloud database companies revenues climbed 35% 12 months over 12 months, whereas multi-cloud database gross sales skyrocketed 531%. Oracle additionally added 10 new multi-cloud areas in the course of the quarter, taking the overall to 55 areas globally. Its AI infrastructure revenues surged 243% 12 months over 12 months, highlighting sturdy demand.

Nonetheless, Oracle’s fast growth comes with rising monetary stress. The corporate reaffirmed plans to spend practically $50 billion in capital expenditures for fiscal 2026 because it races to construct AI infrastructure capability quick sufficient to fulfill demand from enterprises and hyperscalers.

The spending surge is forcing Oracle to rely closely on exterior financing. By the tip of the third quarter of fiscal 2026, the corporate had already raised $30 billion by debt and most popular inventory choices. It additionally plans to boost further capital by an fairness program price as much as $20 billion.

The priority is that Oracle’s money stream has turned deeply detrimental. Third-quarter fiscal 2026 free money stream stood at detrimental $24.74 billion, whereas free money stream for the primary 9 months of fiscal 2026 was detrimental $43.8 billion. Though Oracle’s AI alternative is huge, the corporate’s aggressive spending and rising leverage improve execution and monetary dangers.

Salesforce vs. Oracle: Progress Outlook

Each Salesforce and Oracle are positioned to learn from rising enterprise AI spending, however Oracle presently seems to have stronger near-term income momentum due to surging AI infrastructure demand.

The Zacks Consensus Estimate initiatives Oracle’s fiscal 2026 revenues and EPS to develop 17.1% and 23.7%, respectively. For fiscal 2027, revenues are anticipated to leap one other 32.4%, though EPS development is projected at a extra average 7.2%.

Salesforce’s projected development is slower however arguably extra secure. Fiscal 2027 estimates name for income development of 10.9% and EPS development of 5%. Fiscal 2028 revenues and EPS are anticipated to extend 9.3% and 11.7%, respectively.

Whereas Oracle’s AI infrastructure enterprise is presently rising quicker, Salesforce might provide a extra balanced development profile supported by recurring software program revenues, stronger margins and decrease monetary threat.

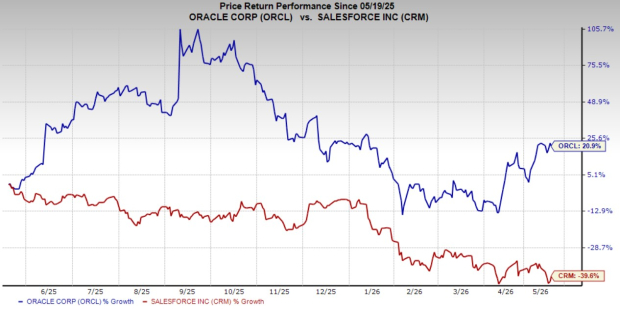

CRM vs. ORCL: Worth Efficiency & Valuation Verify

Over the previous 12 months, Salesforce shares have declined 39.6%, whereas Oracle inventory has gained 20.9%, reflecting investor pleasure round Oracle’s AI infrastructure alternative.

Picture Supply: Zacks Funding Analysis

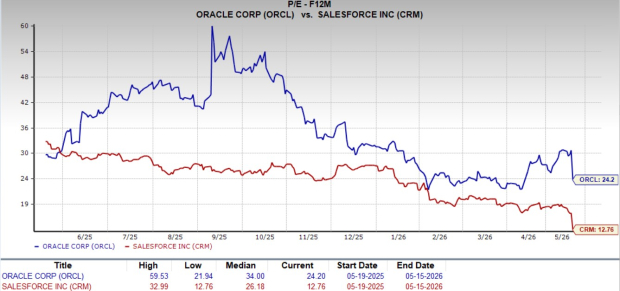

Regardless of weaker inventory efficiency, Salesforce now seems much more enticing from a valuation perspective. The inventory trades at a ahead 12-month price-to-earnings a number of of 12.76, considerably under Oracle’s 24.2.

Picture Supply: Zacks Funding Analysis

Conclusion: Salesforce Seems to be Just like the Higher Wager Proper Now

Oracle clearly has stronger short-term development momentum, notably in AI infrastructure and cloud computing. The corporate is benefiting from explosive enterprise demand for AI workloads, and its multi-cloud technique is gaining traction quickly.

Nonetheless, a lot of that optimism already seems mirrored in Oracle’s valuation. Extra importantly, Oracle’s aggressive spending plans, rising debt ranges and deeply detrimental free money stream introduce significant monetary dangers that traders shouldn’t ignore.

Salesforce, alternatively, provides a extra balanced funding story. The corporate continues to develop steadily, increase its AI ecosystem and generate sturdy earnings development with out inserting main stress on its steadiness sheet. Its rising success with Agentforce and Information Cloud additionally reveals that Salesforce is changing into a critical AI platform participant, not only a buyer relationship administration software program firm.

With a considerably cheaper valuation, more healthy monetary profile and increasing AI monetization alternatives, Salesforce seems to supply a greater risk-reward setup than Oracle at present ranges. For long-term traders on the lookout for publicity to enterprise AI and cloud software program, Salesforce looks like the stronger purchase proper now.

Presently, Salesforce has a Zacks Rank #2 (Purchase), making the inventory a must-pick in contrast with Oracle, which has a Zacks Rank #3 (Maintain). You may see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.